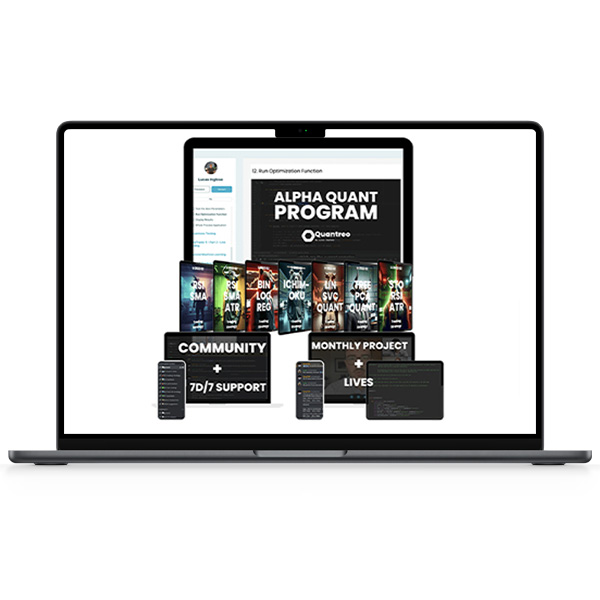

Unlock the Power of Quantitative Finance with the Alpha Quant Program by Lucas Inglese

In today’s rapidly evolving financial markets, quantitative finance and algorithmic trading are essential skills for anyone looking to thrive in the industry. The Alpha Quant Program by Lucas Inglese offers a comprehensive and practical education in these critical areas, equipping participants with the knowledge and tools needed to excel as quant traders, portfolio managers, or financial engineers.

Whether you’re a beginner or an experienced professional, this course provides a deep dive into the world of quantitative finance, covering everything from the fundamentals of algorithmic trading to advanced strategies in high-frequency trading.

Why Choose the Alpha Quant Program?

Lucas Inglese, a leading expert in quantitative finance and algorithmic trading, has designed the Alpha Quant Program to provide a robust, industry-relevant curriculum. With years of experience in the financial markets, Lucas brings knowledge and practical insights reflected throughout the course. This program is ideal for those who want to develop a solid understanding of quantitative finance and apply algorithmic trading strategies effectively in real-world scenarios.

Course Overview

The Alpha Quant Program course is structured to offer a comprehensive education in quantitative finance. It covers the key areas necessary for understanding and implementing successful trading strategies. Below is a detailed breakdown of the program’s core modules.

Introduction to Quantitative Finance

What is Quantitative Finance?

Quantitative finance uses mathematical models, statistical techniques, and algorithms to analyze financial markets and develop trading strategies. This module provides an overview of quantitative finance and its significance in today’s financial markets.

Why Is Quantitative Finance Important?

Understanding quantitative finance is crucial because it allows traders and investors to make data-driven decisions, optimize their portfolios, and develop strategies that can perform well under various market conditions. This module introduces participants to the principles of mathematical modelling, statistical analysis, and their applications in finance.

Fundamentals of Algorithmic Trading

What Is Algorithmic Trading?

Algorithmic trading refers to the use of computer algorithms to automate trading decisions, allowing for faster and more efficient trade execution. This module provides a comprehensive introduction to algorithmic trading, including its advantages over traditional manual trading.

How Do You Build an Algorithmic Trading System?

Participants will learn about the components of algorithmic trading systems, including data collection, strategy development, backtesting, and execution. The course also covers the various platforms, APIs, and programming languages commonly used in the industry, such as Python and R.

Data Analysis and Quantitative Modeling

How Important Is Data Analysis in Quantitative Finance?

Data analysis is the backbone of quantitative finance. This module teaches participants how to collect, clean, and analyze financial data using programming languages like Python or R. The focus is on building quantitative models that can forecast asset prices, volatility, and other key financial metrics.

What Techniques Are Used for Predictive Modeling?

Participants will explore various statistical techniques, machine learning algorithms, and time series analysis methods used for predictive modelling in financial markets. This knowledge is crucial for developing models that accurately predict market movements and inform trading decisions.

Portfolio Optimization and Risk Management

How Do You Construct an Optimized Portfolio?

This module focuses on strategies for constructing diversified portfolios that align with risk-return objectives. Participants will learn about various asset allocation and portfolio optimization techniques, ensuring that their investments are balanced and strategically managed.

What Are the Best Practices for Managing Risk?

Effective risk management is key to long-term success in trading. The course covers essential risk management techniques, including value-at-risk (VaR), conditional value-at-risk (CVaR), and stress testing. Participants will also learn about stop-loss orders, position sizing, and hedging strategies to protect their portfolios.

Algorithmic Trading Strategies

What Are Some Popular Algorithmic Trading Strategies?

In this module, participants will explore algorithmic trading strategies, such as mean reversion, trend following, statistical arbitrage, and machine learning-based approaches. Understanding these strategies is vital for developing a diversified trading approach.

How Do You Test and Optimize Trading Strategies?

Backtesting is an essential part of strategy development. The course teaches participants how to backtest their trading strategies using historical data to assess performance and profitability. It also covers optimization techniques, including parameter tuning, strategy refinement, and robustness testing.

High-Frequency Trading (HFT) and Market Microstructure

What Is High-Frequency Trading?

High-frequency trading (HFT) involves executing large orders at extremely high speeds, often within fractions of a second. This module explains the mechanics of HFT and its impact on market liquidity, price discovery, and market efficiency.

How Do You Develop High-Frequency Trading Strategies?

Participants will learn about market microstructure concepts, such as order types, market impact, and order book dynamics. The course also covers techniques for developing and implementing high-frequency trading strategies while managing execution risks.

Algorithmic Trading Infrastructure and Technology

What Infrastructure Is Needed for Algorithmic Trading?

Algorithmic trading requires a robust infrastructure that includes hardware, software, connectivity, and co-location services. This module provides an overview of the necessary infrastructure components for low-latency trading.

How Do You Optimize Latency in Trading Systems?

Latency optimization is critical for algorithmic trading success. Participants will learn about network architecture, proximity to exchanges, and other factors influencing latency. The module also covers evaluating and selecting trading platforms, execution brokers, and market data providers for optimal performance.

Regulation and Compliance

What Are the Regulatory Requirements for Algorithmic Trading?

Algorithmic trading is subject to stringent regulations to maintain market integrity and protect investors. This module explains the regulatory frameworks and compliance requirements for algorithmic trading, including Reg NMS, MiFID II, and MAR.

How Do You Ensure Compliance in Trading Activities?

Participants will learn how to implement internal controls, monitoring systems, and audit trails to demonstrate regulatory compliance. Understanding these aspects is essential for operating within legal boundaries and avoiding penalties.

Backtesting and Performance Evaluation

How Do You Conduct Robust Backtesting?

Backtesting is a critical step in validating trading strategies. This module teaches participants how to conduct robust backtesting to assess performance and validate assumptions.

What Metrics Are Used to Evaluate Strategy Performance?

The course covers performance metrics such as the Sharpe ratio, maximum drawdown, and alpha-beta coefficients, which are used to evaluate the effectiveness of trading strategies. Participants will also learn how to incorporate transaction costs, slippage, and market impact into backtesting simulations for realistic performance estimation.

Who Should Enroll in the Alpha Quant Program?

The Alpha Quant Program course is designed for a wide range of participants, including:

- Aspiring Quant Traders: Individuals looking to enter the field of quantitative finance and algorithmic trading.

- Portfolio Managers: Professionals seeking to enhance their portfolio management skills with quantitative techniques.

- Financial Engineers: Experts interested in applying advanced mathematical models to financial markets.

- Seasoned Traders: Experienced traders aiming to refine their strategies and stay competitive in the market.

Why Is This Course Worth Your Time?

The Alpha Quant Program course by Lucas Inglese offers more than just theoretical knowledge—it provides practical skills that can be directly applied in the financial markets. With a focus on real-world applications, participants will leave the course equipped with the tools and strategies needed to succeed in the competitive world of quantitative finance and algorithmic trading.

Conclusion

The Alpha Quant Program is an essential course for anyone serious about mastering quantitative finance and algorithmic trading. Whether you’re just starting or looking to deepen your expertise, this program offers a comprehensive curriculum covering all field aspects. From data analysis and quantitative modeling to advanced trading strategies and regulatory compliance, the course prepares you to navigate the complexities of modern financial markets with confidence and precision.

Enroll in the Lucas Inglese – Alpha Quant Program today and take the first step towards becoming a successful quant trader in today’s fast-paced financial markets.

Original price was: $299.00.$20.00Current price is: $20.00.

Sale!

Original price was: $299.00.$20.00Current price is: $20.00.

Sale!

Original price was: $997.00.$20.00Current price is: $20.00.

Sale!

Original price was: $997.00.$20.00Current price is: $20.00.

Sale!

Original price was: $15,000.00.$38.00Current price is: $38.00.

Sale!

Original price was: $15,000.00.$38.00Current price is: $38.00.

Sale!

Original price was: $1,491.00.$24.00Current price is: $24.00.

Original price was: $1,491.00.$24.00Current price is: $24.00.